Non-financial audits of companies will soon require regular reporting on sustainability information relating to the company’s impact on the environment, communities and people, with governance, including cybersecurity, included. Beginning in 2025, ESG reporting will become mandatory at the earliest for select public interest organizations.

The concept of ESG was coined in 2005 to incorporate Environmental, Social and Governance principles into the criteria for evaluating companies when investing in the capital markets. This allowed investors to decide whether to invest their money in companies whose activities have a negative impact on the environment. As ESG ratings are provided by several rating agencies, such as MSCI ESG Research, Sustainalytics or ESGI, which have different assessment methodologies, the ratings lacked uniform rules.

The European Union’s decision to introduce transparency in ESG and also to support Europe’s move towards sustainability has brought new directives that introduce regulated rules for organisations to act responsibly towards the environment and society. Criteria related to corporate governance are also being taken into account, and banks and investors have been interested in the impact of organisations on serious global issues for a long time and increasingly so. A new indicator can thus clearly differentiate a company in a competitive environment, which is why ESG investments are also of increasing interest.

“As large customers and banks now require some of the sustainability data as well, publishing information on the sustainable behaviour of a company is not a novelty,” explains the Commercial Director of GAMO a.s. Zuzana Holý Omelková. “In the first step, it is essential to know the current state of the company in order to initiate the necessary changes for the ESG rating,” she adds.

Who is affected by ESG?

The ESRS European Sustainability Standards have been in force since January 2024 and form the basis of legislation for around 700 large companies in Slovakia. From 2025, the obligation to publish an ESG report will apply to public interest organisations with more than 500 employees. In 2026, companies that meet at least two of the following three criteria: assets worth more than EUR 20 million, a net turnover of more than EUR 40 million, or more than 250 employees. ESG reporting will then also be mandatory from 2027 for SMEs listed on EU regulated markets, and in 2029 also for third country entities with at least one subsidiary or branch in the EU and a net turnover of more than €150 million.

So where to start?

To obtain an ESG score, a company must start by collecting and processing a vast amount of data from areas as diverse as HR, energy supply or manufacturing, including information on sustainable cybersecurity practices. “Our goal is to fully collaborate with companies to address sustainability issues,” says GAMO Inc. database specialist Roman Schmidt, adding that “we can optimally unify the generated data to create a comprehensive software tool for a company’s holistic view of the ESG data we collect.”

The preparation of the sustainability report is governed by the Accounting Act in Slovakia. The most time-consuming phase is the initial analysis and data collection phase and consultation on relevant content. “The processes therefore noWe are increasingly incorporating modern elements of artificial intelligence, which is becoming an essential part of IT life. We are getting more accurate data predictions from every area of the business and such a comprehensive software tool provides a detailed overview of the audited ESG data,” adds Roman Schmidt.

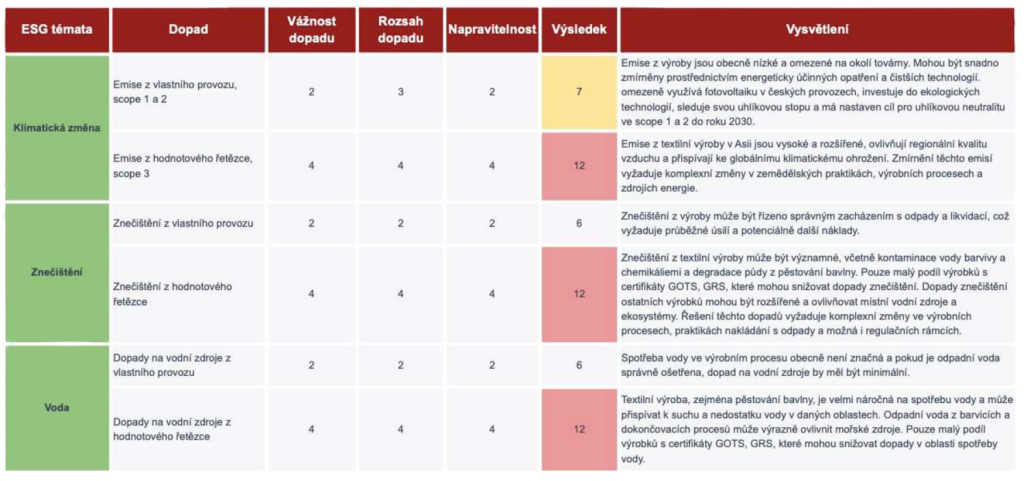

The data collection covers three areas

As ESG stands for Environment, Social and Governance, it encompasses these three thematic areas when collecting and evaluating data relevant for reporting. Environment, ESRS standards E1 to E5, relate to climate change, pollution, water and its resources, biodiversity and ecosystems, and circular economy. Social includes standards S1 to S4, which represent a responsible and humane approach to employees, affected communities or consumers. However, developing an agenda for governance, i.e. Governance, is key to a company’s success. It also includes issues of cyber security and cyber threat management, the growth of which is increasingly impacting the business, operations, continuity and reputation of firms. “Managing the threats that can be associated with the failure to detect industrial, manufacturing and security systems as a result of hackers taking control, or following a ransomware attack, will ensure the health and business future of any organisation. It will also protect the interests of customers, clients and business partners,” explains Zuzana Holý Omelková, a cyber security expert.

Source.

Source: SUSTO Sustainability Tools

ESG target setting

Defining targets and key performance indicators, along with setting company-wide sustainability management, is the next stage of the ESG process. “In any one corporate environment, we can deploy not only reporting tools for reporting, but also analytical tools to identify opportunities for meeting ESG goals towards sustainability and efficiency,“ says Roman Schmidt of GAMO. This phase entails thorough strategic planning and involves the development of a sustainability reporting roadmap, which depends on the approach used, the tools, the timeframe chosen and the size of the company.

ESG report

Primary sector analysis will therefore ensure that content and input from a variety of sources is processed, with decision-makers and experts identifying the topics that are most relevant to the sector. The company then involves stakeholders – employees, management, suppliers and customers – in the data collection process by completing an ESG questionnaire. Based on the findings from the questionnaires, a scoring process takes place to determine the severity of the impacts observed, their extent and possible remediation. The impacts then need to be categorised according to the identified methodology for analysis and the resulting scores numerically into important, significant and critical.

Similarly, the relevance in terms of the financial impacts or risks of the enterprise should be assessed separately in each of the three ESG topic areas. These assessments serve as the basis for developing the resulting list of materiality thresholds for impacts and risks. The identified materiality areas then serve as the basis for setting targets for improvement and monitoring of the company’s activities, as well as for developing the ESG strategy.

Opportunities for Slovak companies

The application of ESG standards varies from industry to industry. Many Slovak companies are already introducing sustainable measures today, which may include replacing their fleet with electric vehicles, reducing production waste or recycling it. However, a frequent problem is the lack of capacity to self-sustain the whole process . “We can also use our years of experience in developing various technology solutions to set up data collection and reporting processes for sustainable, responsible and ethical business,” says Zuzana Holý Omelková. The company has also joined forces with experts oriented in the key topics of sustainable development. By collaborating with the consulting company SUSTO Sustainability Tools, GAMO wants to help customers build resilient businesses for a sustainable future and deploy effective ESG software tools in every corporate environment.